2025 was a record year for battery energy storage systems (BESS) in Germany: more storage capacity was added than ever before. The market for stationary battery storage in Europe’s largest economy is booming – and there is no sign of this trend slowing down.

At the same time, there are also several challenges for both existing and future battery storage projects in Germany. Reason enough to take a closer look at the German BESS market.

Status quo: Where does the German BESS market stand?

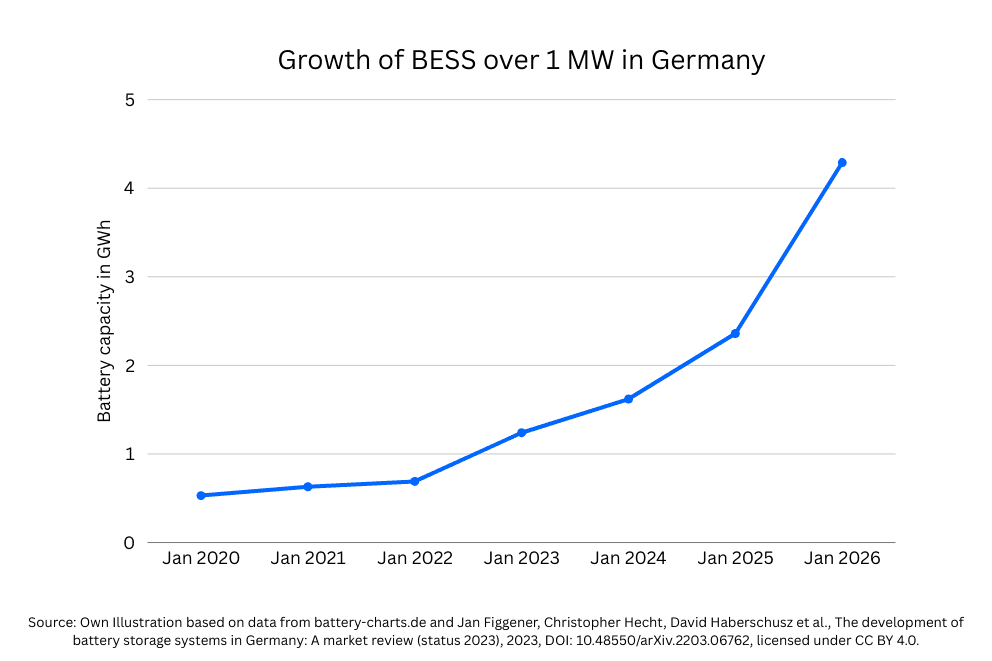

According to the German Federal Network Agency (Bundesnetzagentur, or: BNetzA), as of October 2025 Germany has grid-scale battery storage systems (defined as systems with a capacity above 999 kW) with a total installed gross power of 2.4 GW and 3.2 GWh of storage capacity. Hundreds of projects with a combined capacity of 5 GW and 10.4 GWh are currently in development.

In 2025 alone, 842 MW of storage capacity were added according to Modo Energy – almost twice as much as in the previous year. After a relatively late start, Germany has now become Europe’s most attractive market for BESS, ahead of the UK and Italy, says Aurora Energy Research.

BNetzA expects total installed capacity to grow to around 41 GW by 2037 – almost twice the level projected just two years ago.

These figures speak for themselves: battery energy storage systems are no longer a niche technology in Germany but a system-relevant component of the energy system – and a strong structural signal for investors and operators.

Why are BESS booming in Germany?

Several reinforcing factors are driving the rapid growth of BESS in Germany.

Energy transition and growing demand for flexibility

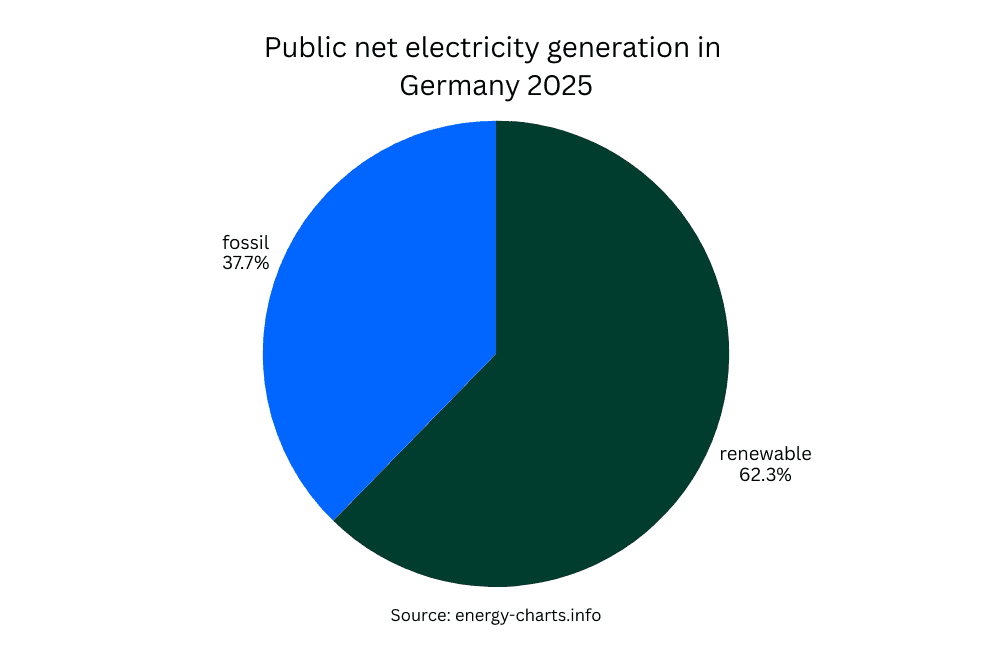

Since the introduction of the Renewable Energy Sources Act (German: Erneuerbare-Energien-Gesetz, or: EEG) in 2000, Germany has consistently expanded renewable electricity generation. Data from 2025 show that renewables now account for the largest share of the German electricity mix.

Just ten years ago, the situation looked very different: roughly two-thirds of electricity came from fossil fuels, while only one-third came from renewables. Since then, the energy system has undergone a profound structural transformation.

However, Germany’s energy transition is far from complete. The country aims to generate 80% of its electricity generation from renewable sources by 2030. The more wind and solar power is integrated into the grid, the greater the need for fast-responding flexibility – a role that BESS are particularly well suited to provide. German energy esearch institute Fraunhofer ISE estimates a storage demand of 100 to 170 GWh by 2030.

Increasing volatility in the power market

As the share of renewable energy grows, electricity generation becomes increasingly volatile. In 2025, Germany recorded almost 575 hours of negative electricity prices, according to energy research institute FfE – significantly more than the previous record in 2024 (459 hours).

This increases the need for flexibility, local grid relief, and system services. At the same time, this volatility forms the economic foundation of every battery energy storage system.

Declining hardware costs

Since 2010, the cost of lithium-ion batteries has fallen by more than 75%. Today, LFP technology (lithium iron phosphate) dominates the market, offering lower costs, higher stability, and improved safety compared with older NMC chemistries.

Lower capital costs shorten payback periods and make an increasing number of projects economically viable.

Revenue streams: How do BESS make money in Germany?

For battery storage operators, the key question is revenue generation. The German market offers several potential income streams.

Frequency Containment Reserve (FCR)

Frequency Containment Reserve (FCR) has long been the dominant revenue model for battery storage in Germany. BESS can respond to frequency deviations within 30 seconds and receive a capacity payment in return.

However, the market is showing clear signs of saturation: the amount of FCR capacity provided by batteries continues to grow while overall demand from transmission system operators remains stable. Operators who rely exclusively on FCR risk leaving significant revenue potential untapped.

Automatic Frequency Restoration Reserve (aFRR)

Automatic Frequency Restoration Reserve (aFRR) has become Germany’s largest balancing market in terms of TSO expenditure, making it particularly attractive for battery storage systems.

As conventional power plant capacity declines, the supplier structure is gradually shifting toward faster and more flexible technologies. Since BESS do not yet dominate this market, attractive revenues can still be achieved.

Unlike FCR, aFRR includes two revenue components: a capacity payment and an energy payment when the reserve is activated. Both payments apply separately to positive and negative balancing services. As conventional plants exit the market, battery participation in aFRR continues to grow. Operators who leverage aFRR strategically can benefit from one of the strongest revenue streams in the German market.

Day Ahead Arbitrage

In the day-ahead market, electricity is traded for delivery the following day. Battery storage systems purchase electricity during periods of low prices – typically during high solar or wind generation – and discharge when demand and prices are higher.

The price spread forms the margin. Since the day-ahead auction closes at 12:00 PM each day, storage dispatch can be planned and optimized algorithmically. As volatility in the wholesale electricity market increases, this strategy becomes increasingly attractive.

Intraday Arbitrage

Germany has one of the most liquid and volatile intraday electricity markets in Europe: around 15–20% of total power trading takes place there. Two trading formats can be distinguished: the intraday auction, which takes place several times a day, and continuous intraday trading (Intraday Continuous). Increasing wind and solar generation, short-term price movements, and forecast updates create daily price spreads that battery energy storage systems can systematically exploit.

Revenue Stacking

The highest revenues are typically achieved by operators who do not rely on a single market but combine multiple revenue streams. In revenue stacking, algorithms determine in real time which market offers the highest value and dispatch the battery accordingly.

This requires precise forecasts, technological expertise, market access, and advanced optimization software. As a result, many operators outsource this task to specialized battery optimizers such as The Mobility House Energy.

Redispatch

When congestion occurs in the electricity grid, system operators must intervene by reducing generation in one location and increasing it elsewhere.

Since 2021, all assets with a capacity of 100 kW or more can be integrated into this redispatch process, including BESS. Grid operators compensate participants for providing flexibility, creating an additional revenue stream within the overall revenue stack.

What challenges does the German BESS market face?

While the German electricity market provides favorable conditions for BESS projects, several regulatory uncertainties remain.

1) Grid connections

Despite strong investor interest, grid connection remains the biggest operational bottleneck for BESS projects in Germany. Transmission system operators currently report around 650 grid connection requests, and approval processes often take several years.

2) Grid fees

When a BESS charges electricity from the grid, it is legally classified as a final consumer, meaning grid fees normally apply. However, no grid fees are charged when electricity is fed back into the grid.

Battery storage systems commissioned before August 2029 benefit from a 20-year exemption from grid fees under Section 118(6) of the German Energy Industry Act (EnWG). This rule has been one of the key economic incentives driving the current boom.

Whether this exemption will be extended remains uncertain. The German Federal Network Agency is currently reviewing the overall grid fee system, as grid fees have accounted for an increasingly large share of electricity prices in recent years.

Update: In late May 2026, the Bundesnetzagentur announced that the grid fee exemption will expire as planned but will not be terminated early. In the future, storage systems will contribute to grid financing through a moderate capacity charge, while energy-based charges will not apply. This applies to storage systems whose final investment decision (FID) is made after the regulation enters into force (expected in early 2027).

3) Grid reform package

The German government is also working on a comprehensive grid reform package aimed at restructuring grid connection procedures and addressing rising redispatch costs.

A draft proposal published in early 2026 includes new instruments for grid operators as well as simplified rules for co-located battery storage systems.

4) Planning law for projects outside urban areas

BESS with a capacity above 1 MWh were recognized as privileged infrastructure in rural planning zones at the end of 2025. However, the regulation was quickly tightened.

The privilege now only applies to co-located storage systems connected to renewable generation and to stand-alone storage above 4 MW that meet specific location criteria, such as proximity to substations or power plants. Critics warn that these changes could create new planning hurdles and land-use conflicts.

Outlook: How will the German BESS market evolve?

The structural drivers behind BESS growth remain intact: increasing renewable generation, higher price volatility, and growing demand for flexibility.

Short-term developments (2026)

Two regulatory developments are likely to shape the market in the near term.

First, Germany has introduced a market for instantaneous reserve, a new revenue segment that battery systems can potentially participate in.

Instantaneous reserve stabilizes grid frequency within a time window ranging from milliseconds up to 30 seconds, bridging the gap before primary control reserves activate. For BESS, this means they can now be compensated for providing system-stabilizing inertia services – not a game changer, but an additional revenue stream.

Second, regulation on the market integration of storage and charging infrastructure (referred to as MiSpeL in German) is expected to come into force in mid-2026. It will allow hybrid storage systems in co-location to charge both renewable electricity and grid electricity without losing eligibility for EEG support.

Medium-term developments (from 2028)

Germany is also planning to introduce a capacity mechanism around 2028.

In countries with established capacity markets, such as the UK and Italy, battery storage projects regularly receive capacity payments that provide predictable revenue streams. A similar mechanism in Germany could significantly improve the bankability of BESS projects and facilitate project financing.

Regulatory outlook

At the same time, the evolution of the regulatory framework remains crucial. Both the upcoming EEG reform and the planned grid reform package will play a key role in shaping the investment and operating environment for battery storage systems in Germany in the coming years.

Conclusion: The German BESS market is growing – and becoming more complex

Germany is one of the most volatile electricity markets in Europe and therefore a structurally attractive environment for battery energy storage systems. In a short period of time, the industry has not only grown significantly but also become increasingly professionalized.

However, as the market expands, complexity increases. Regulatory uncertainty, diversified revenue streams, and rising optimization requirements make professional expertise essential. Operators who want to succeed in this market need access to advanced optimization technology, deep market knowledge, and partners capable of maximizing revenue performance.